What if You Always Maxed Out Your 401k?

What’s the surest way to become a millionaire? I can tell you right now – max out your 401k contribution every year. It will take a while, but I guarantee you will get there. This is the easiest way to build wealth. The problem is you have to start investing young and most of us didn’t know that when we were 22. We all spent too much money and didn’t invest enough in our 20s. Even I didn’t want to contribute to my 401k when I started working in 1996. To that young guy, retirement was 40+ years away. Why should I put so much money aside? I wanted to go out, have fun, replace my junky old car, and buy nice clothes. Fortunately, my dad convinced me to start contributing to my 401k and saved me from a huge mistake. The compounding effect of investing early is absolutely amazing. It’s too bad so many young people don’t understand this concept and put off investing until later.

Woefully inadequate retirement savings

Putting off retirement savings is a big mistake. If you don’t start saving right away, it can be very difficult to put money away. Can you believe that half of all US households have no retirement savings at all? It’s true. Even households that saved for retirement haven’t saved enough. According to the latest (2019) Survey of Consumer Finance, the median value of retirement accounts for families near retirement age is $134,000. That’s only the people with retirement accounts. People with no retirement accounts have much less savings.

Anyway, even $134,000 won’t be enough to support a frugal retirement. If you keep track of your annual expenses, you’d know. For us, $134,000 would cover about 3 years of modest living. That’s not long enough. Many people spend 30+ years in retirement. What will they do once their savings are gone? They will have to depend on other sources of income such as Social Security Benefits and part-time work. Unfortunately, this usually means drastically downgrading their lifestyle.

Luckily, I’m not average and you aren’t either. If you’re reading this, you’re way ahead of the average household.

I have been maxing out my 401k for many years now and my retirement savings are in great shape. Let me show you how wealthy you’d be if you maxed out your 401k contribution every year since you started working. Hold on tight because you will be amazed by the power of compounding*.

*Compounding is just another word for compound interest.

Maxed out 401k every year

The graph below shows how much your 401k would be worth if you maxed out your contribution every year.

Note: In our scenario, I have our worker contribute the max contribution divided by 12 every month. To make it simple, we’ll invest in VFINX, the Vanguard S&P 500 index fund. (This doesn’t include any employer contributions. You should be ahead of this chart if your employer helped out.)

Here is how to read this graph.

- The horizontal axis is how many years you have been working.

- The green line is how much your 401k would be worth if you maxed out every year.

- The blue line is how much you contributed.

For example: If you started working in January 2012, then that’s 10 years you could have invested in your tax-advantaged account. If you contributed the max every year, then you should have about $400,000 in your 401k account by now. 2021 was a terrible year for many people, but the stock market had another amazing run. If you invested for many years, all your investment got a huge boost. That’s compounding in action.

My 401k

I’ve been working since mid-1996 so let’s round down to 25 years. If I maxed out every year and invested in VFINX, then I should have about … $1,453,000 in my 401k at the end of 2021. Unfortunately, my account doesn’t have that much. I made some mistakes when I was young, like most people. I didn’t max out my 401k contribution when I first started working. It took me a few years to increase my contribution to the maximum allowed. Also, I chased performance in my early 20s. That meant my investments underperformed in those crucial early years.

At the end of 2021, I had about $1,020,000 in my 401k. That’s closer to 18 years of work instead of 25. Those early mistakes got amplified as the years go by. If I could go back, I’d tell my younger self to focus on maxing out the 401k and put everything in a good index fund. My dad told me to invest in my 401k, but he didn’t know about index funds. I had to learn the hard way from my mistakes. I’m still thankful that he convinced me to invest in my 401k. You can read more about my mistakes below.

How is your 401k doing?

The full table is below. It’s very easy to use. You just need to look at the first column and find the number of years you’ve worked. The Accumulated Value column shows how much your 401k would be worth if you’ve maxed out your contribution right from the beginning. The 4th column shows the max contributions for the corresponding years.

You can see the magic of compounding on this table. If you contributed $7,313 in 1988, it would turn into $201,273 today! That’s an incredible 2,751% gain AND it will keep increasing every year. Time is your best ally when it comes to investing.

It is clear that maxing out your 401k will make you wealthy by the time you retire. If you did and started working before 2000, you would be a millionaire now. I love my 401k and I can’t wait for it to hit 7 figures someday. Unfortunately, most workers aren’t contributing enough and that’s why the median value of retirement accounts is so low.

*Woohoo! My 401k finally crested over a million dollars. I’m officially a 401k millionaire! Although, stocks have gone down lately. My 401k accounts are worth less than a million again…

Lessons learned

- Don’t delay maxing out your contributions. It took me a few years before I maxed out my 401k contributions. Those early years are crucial and you need to max out ASAP. The longer you wait, the more you’ll lose out with compounding.

- Don’t chase performance. I didn’t know how to invest when I was younger and I just picked the funds with the best performance from the previous year. This is called chasing performance. This is a bad idea and it will underperform in the long run. Funds that did very well the previous year usually underperform the next. It is better to invest in a low fee index fund like VFINX and just keep adding more every month.

- Don’t pause investing. I stopped investing for a while after the Dot Com bubble busted. This worked out okay in the short term because the market kept going down. However, it was the wrong move in the long term. If I kept investing, my retirement fund would be worth much more today. You need to keep contributing even during a stock market crash. I learned that lesson and kept investing in 2020. It paid off handsomely.

- Don’t borrow from your 401k. I haven’t done this because I never had to. It’s the wrong move because your retirement fund will be depleted and you’ll miss out on compounding. Your retirement accounts should be earmarked for retirement.

Those are the main lessons I learned from 24 years of investing in my retirement account. I hope these lessons will prevent some young investors from making similar mistakes.

Max out your 401k

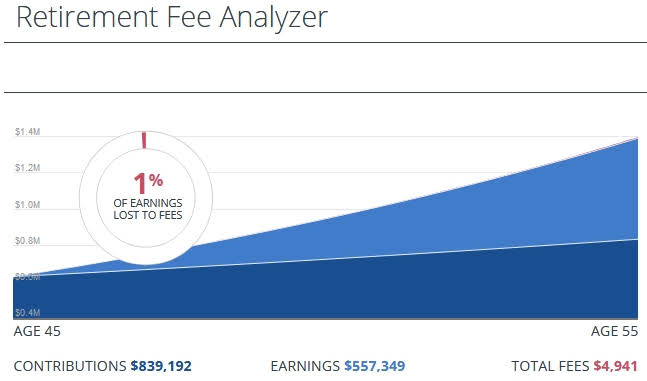

Of course, every 401k plan is different. Your retirement plan might not have any good investment or the fees might take a huge bite out of your total return. Here is an easy way to see how much fee you are paying – sign up with Personal Capital and use their 401k fee analyzer tool. This free tool will help you figure out how much you’re paying. I just checked my 401k and I’ll pay almost $5,000 in fees by the time I’m 55. That sounds like a lot, but it is actually very low. All my investments are in low-cost index funds. Anyway, if you’re paying too much in fees, you probably should move your investment over to funds with lower fees.

For most people, maxing out your 401k contribution every year is the easiest way to become a millionaire. You will pay less tax and you won’t leave any employer matching on the table. As a bonus, the contribution is auto deducted so you won’t even miss the money. Start investing while you’re young and the magic of compound interest will supercharge your 401k and ensure a comfortable retirement. Don’t wait until you’re 55 to start investing because it will be nearly impossible to catch up.

How are your 401k accounts compared to my table? Are you ahead or behind?

If you need help keeping track of your finances, sign up with Personal Capital to manage your portfolio. They have many great tools for investors including the 401k Fee Analyzer and the best retirement calculators on the internet. I log in almost every day to check on my accounts.

Passive income is the key to early retirement. This year, Joe is investing in commercial real estate with CrowdStreet. They have many projects across the USA so check them out!

Joe also highly recommends Personal Capital for DIY investors. They have many useful tools that will help you reach financial independence.

Latest posts by retirebyforty (see all)

Editor’s Note: It’s been a while since we’ve mentioned Chief Income Strategist Marc Lichtenfeld’s core investing system, the 10-11-12…

Copyright © 2024 Retiring & Happy. All rights reserved.