Why the Housing Market is More Important than the Stock Market for Most People

Watching the stock market over the last month has not been much fun. And, if you will be relying on savings withdrawals, market downturns can be particularly stressful. You may be looking at delaying retirement, tightening your purse strings, or both.

However, a great post by Ben Carlson on the Wealth of Common Sense blog this week pointed out that the stock market is probably not the most important barometer of financial health for most Americans. That award should go to the the housing market. Home prices and interest rates are the metrics that should worry most middle and low income households.

It is the Very Wealthy Who Own Stocks

It is the already wealthy who stand to gain and lose the most when the stock market goes down, not the majority of Americans.

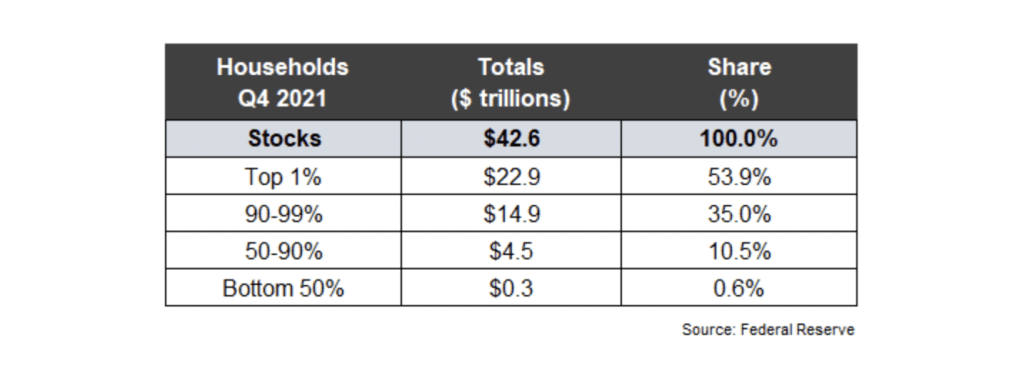

The top 1% of all households own 53.9% of the shares in the markets and the top 10% own nearly 90%. The 50-90% of the households own 10.5% and the bottom 50% own a measly .6%.

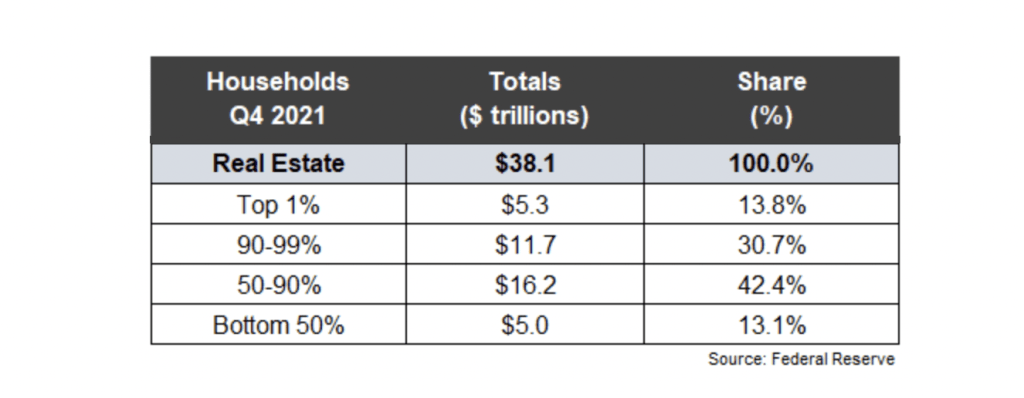

When it comes to real estate, the wealth is more evenly distributed up and down the wealth curve.

The top 10% own less of an overall percentage of the real estate pie. They own 44.5% of real estate (vs. 90% of stocks).

The majority of real estate holdings, 42.4% (vs. 10.5% of stocks), are owned by those in the 50-90% range of all households. And, the bottom 50% own 13.1% of all real estate (vs. .6% of stocks).

The stock market makes the front page and can cause hand wringing by all kinds of people. However, as the data above shows, it is the real estate market that impacts the greatest number of people.

The average mortgage holder in the United States now owns $185,000 in accessible home equity.

CoreLogic reported that in the fourth quarter of 2021, the average homeowner gained approximately $55,300 in equity during the past year.

Hawaii, California, and Washington experienced the largest average equity gains at $128,300, $117,000 and $95,500 respectively. Meanwhile, North Dakota and D.C. experienced the lowest average equity gain in the fourth quarter of 2021 at $16,800 and $11,100 respectively.

Average savings balances are less than a quarter of the average home equity. Americans have a weighted average savings account balance of $41,600 which includes checking, savings, money market and prepaid debit cards.

NOTE: Both savings and home equity balances can vary greatly by age and location. How do you compare? Review average cash, savings, home equity and other balances…

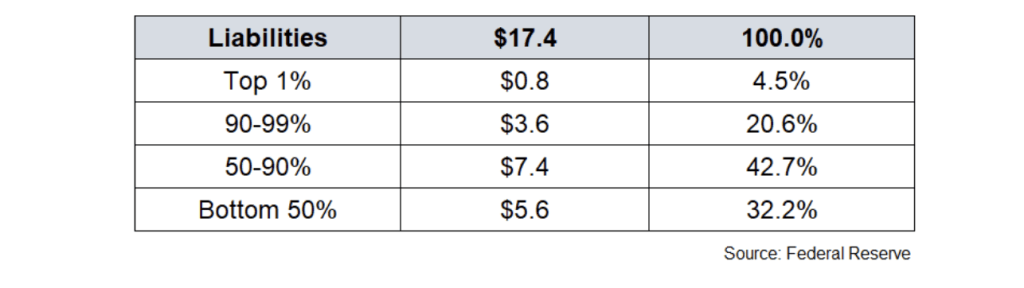

The top 10% holds 70% of the net worth in this country while the bottom 90% accounts for 75% of the debt, largely in home mortgage loans.

Because home equity and mortgages are big components of the balance sheets of the majority of U.S. households, interest rates, inflation, and the health of the housing market are what will have the greatest impact on the financial security of the most number of people.

Let’s explore those metrics:

High home values can continue to bolster the net worth of many households.

And, the home equity can be turned into cash to help cover retirement or other expenses if necessary.

A strong housing market can somewhat make up for low savings rates. Explore ways to cut housing costs or cash in on home equity.

Interest rates are a huge lever since they affect both housing prices and mortgage payments (if you have an adjustable rate mortgage).

When rates rise like they are today, then mortgages rates go up too and people can borrow less which means they can’t pay as much for houses. So, housing prices tend to flatten or in some cases go down.

Similarly for people who have adjustable rate mortgage, when rates go up their mortgage rates and monthly payments can go up which leaves less money for other expenses and saving and investing.

Inflation is definitely hurting middle and low income households who are not seeing their incomes rise in proportion to the the increase in prices.

However, one of the few silver linings of high inflation is that it can benefit those in debt. Debtors gain from inflation because they repay creditors with dollars that are worth less in terms of purchasing power. For example, while you might still owe $100,000 on your mortgage, inflation has caused that $100,000 to be worth less now than it was when you borrowed it.

As Carlson wrote, “considering the bottom 90% holds 75% of household debt and the bottom 50% has roughly one-third of all debt, inflation is disproportionately helping the debts of the middle and lower classes.”

Editor’s Note: Today’s guest column on the potential for a “business bonanza” in 2025 comes from Manward Press Chief…

Copyright © 2026 Retiring & Happy. All rights reserved.