Low Cost Investing: 7 Ways to Slash Your Investment Expenses

Last week, we discussed the fees and expenses to look out for when investing in mutual funds and ETFs. Reducing these fees and expenses is one of the most sure-fire ways to increase your returns without adding any extra risk. As John Bogle, the founder of Vanguard Group, said: “In investing, you get what you don’t pay for. Costs matter.” Follow this guide to low cost investing for simple tricks you can use to reduce your costs. .

Below, we’ll outline 7 ways to keep your investment costs low as you build and preserve your wealth throughout your lifetime.

1. Want Low Cost Investing? Establish a Passive Investment Philosophy

When a passive vs. active investment philosophy is discussed, you may be thinking, “why wouldn’t I want to actively engage in my investment strategy?!” Well, in most cases, it’s more expensive to go all-in on an active management investment philosophy.

An active investor is attempting to beat the stock market whereas a passive investor believes markets are efficient and is trying to capture the returns of a specific sector of the market. If you’re an active investor, your expense ratio (the cost of owning a mutual fund or ETF) will likely be higher since fund managers constantly shift around their stock and bond holdings to try boosting returns.

Meanwhile, a passive investment philosophy consists of:

- Purchasing index mutual funds or ETFs (Exchange-Traded Funds)

- Lowering fees by investing in funds with low expense ratios

- Minimizing risk and taxes through a “buy and hold” approach

A low-cost, tax-efficient (more on that later), investment strategy that you don’t have to fret about year-to-year? Sign me up!

Don’t forget to review the Coach Suggestions in the NewRetirement Planner, where you will receive alerts on specific topics, such as determining if you are an active or passive investor (and why passive is the way to go!).

NOTE: Tune in to this podcast to learn more about the benefits of index investing.

2. Limited Investment Options in Your 401(k)? Consider a Target-Date Retirement Fund

For those of us who are still working, your employer-sponsored retirement plan, such as a 401(k) or a 403(b), is likely one of your primary investment vehicles for retirement savings.

With an employer-sponsored retirement plan, you’re generally limited to the investment options available to you within the plan. For many plans, there are low-cost investment options, like index funds with low expense ratios. However, you still may not want to have to worry about picking the right funds, or choosing the right mix of stocks and bonds, or remembering to rebalance your account from time-to-time.

When you invest in a target-date fund, you don’t need to worry about determining the perfect mix of stocks and bonds or adjusting that allocation over time. The fund will automatically take care of these allocations for you. Also, in most cases, target-date funds are low-cost investment options.

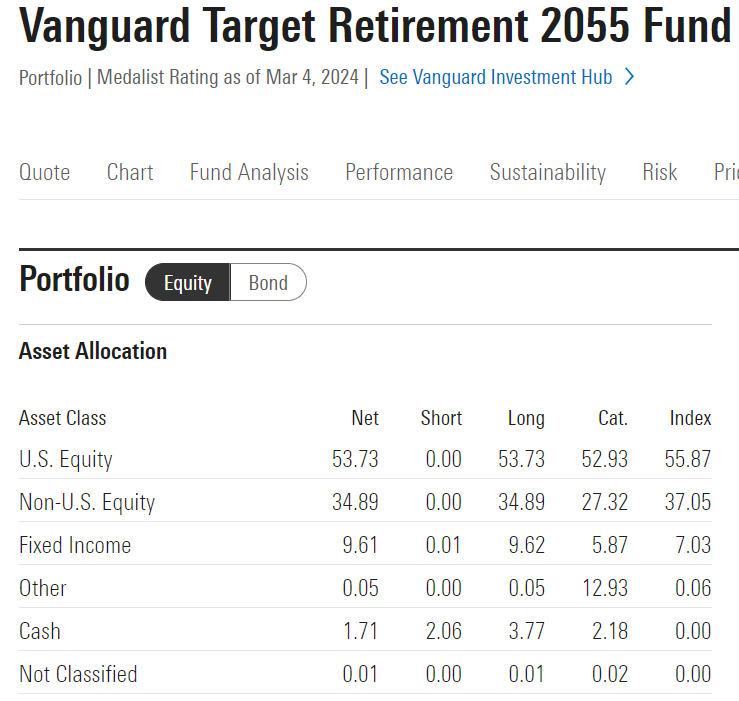

Examining a Target-Date Fund

Let’s take a look at an example of a popular target-date fund: Vanguard Target Retirement 2055 (VFFVX).

If you’re considering retirement around the year 2055, you might opt for that as your target date. As you can see, this one fund is well-diversified with a mix of U.S. stocks, international stocks, some bonds (fixed income) and cash. As you begin to approach 2055, the fund will increase its exposure to bond funds and decrease its exposure to stock funds, becoming more conservative the closer you are to your retirement.

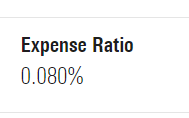

Just as important, this fund has a very low expense ratio of only 0.08%! So, a target-date fund can be a great hands-off, low-cost investment within your employer-sponsored retirement plan, as you don’t have to worry about strategically picking multiple investments or rebalancing on an on-going basis (as this is done for you when investing in a target-date fund).

It is important to note that not all target-date retirement funds are created equally. There can be more costly funds in this category, so be sure to pay attention to the expense ratio before investing into a fund. If there are only expensive target-date funds within your plan (think a 0.30% or higher expense ratio), you may be better off picking a couple of low-cost index funds and taking a more hands-on approach.

3. Assess the Costs of 401(k) Rollover Options

In addition to the fees associated with the particular investments, it’s important to be mindful of any fees associated with the types of accounts in which you’re invested.

This is especially important when you are considering what to do with your 401(k) from a former employer. You essentially have three options:

- Leave your 401(k) as is with your former employer

- Roll over your 401(k) to your current employer-sponsored retirement plan (if you’re still working)

- Roll over your 401(k) to an IRA

When considering whether to leave your 401(k) with your former employer or roll it into your current employer’s plan, it’s essential to assess the investment options and fees within both plans.

Upon leaving a 401(k) account with your former employer, you may encounter administrative charges that were previously covered by your employer during your employment but are no longer covered as a former employee. These could include charges such as bookkeeping, service, and legal fees to manage the account that could reduce your return potential. You should contact your plan administrator or 401(k) provider to determine if these charges would be applicable if you are considering leaving your 401(k) at your former employer.

If you have better investment options in your current plan (think low-cost index funds or target-date funds), then you may be better off rolling that old retirement plan over.

Meanwhile, it may be a better decision from a total cost standpoint to roll over your 401(k) to an IRA. In an IRA, usually the only costs are those of the investments you hold and you have a lot more options than just through your employer-sponsored retirement plan. If your account is small enough or you insist on paper statements, some custodians may charge you a small annual fee.

NOTE: If you make backdoor Roth IRA contributions, you may want to think twice before you roll your old 401(k) into a Traditional IRA due to the pro-rata rule.

Keep track of all of your different types of investment accounts, including former 401(k)s, by ensuring they are all entered and titled correctly in the NewRetirement Planner.

4. Keep it Simple – Avoid The Excitement (& High Costs) of Exotic Investments

At a certain point in your investing journey, especially with more wealth accumulated in your later career years, it may be tempting to invest in something a little more “exciting” than low-cost index funds or ETFs. This may include more “exotic” investments such as private equity, venture capital and hedge funds.

You may be able to afford to invest in these types of investments, but you don’t necessarily need to. What’s even more exciting than investing in these exotic funds, though, is keeping your investment costs low so you can get more out of your investment returns. And these more alternative types of investments are not going to allow you to do so.

Both hedge funds and private equity tend to be more expensive than a typical index mutual fund or ETF. Hedge fund managers typically charge an asset management fee based on the fund’s net assets (generally between 1 and 2%), along with a performance-based fee structured as a share of the fund’s capital appreciation (generally between 15 and 20%, historically). Private equity funds have a similar fee structure consisting of a management fee and a performance fee.

Adding complexity to your investment strategy doesn’t guarantee anything, other than typically higher costs. Keep it simple!

5. Minimize Account Maintenance and Trading Fees

You may be saving money by not utilizing a financial advisor to assist with your investments, but there are also fees to watch out for as a DIY investor.

Full-service, or traditional, brokerages often charge fees to maintain your accounts. For example, Edward Jones charges an annual account fee of $75 for a Traditional or Roth IRA. You may want to stick with major online brokerages – such as Charles Schwab or Fidelity, as examples – which typically don’t charge account maintenance fees.

There isn’t a standardized system for trading commissions or additional fees imposed by brokerage firms and other investment institutions. Certain firms may impose substantial fees per trade, whereas others have minimal charges, often reflecting the extent of services offered.

Consider investing your money with a firm that charges no commissions or fees for stock and ETF trades.

Of course, if you follow a passive, buy-and-hold investment strategy, frequent trading won’t be a concern anyway!

6. Taxes Are a Cost Too! Reduce Your Investment Taxes

Along with the actual investment fees and expenses, taxes are also a cost to consider when investing. Let’s take a look at some ways in which you can lower your investment taxes.

Passive Investing Equals Tax-Efficient Investing

If you are investing in a taxable brokerage account, a passive investment strategy of index mutual funds and ETFs with built-in tax efficiency can minimize the tax drag on your returns.

These funds are tax-efficient because they have a low turnover ratio, which is the percentage of a fund’s holdings that have been replaced in the previous year, leading to taxable capital gains. ETFs may offer an additional tax advantage: The ETF redemption process sometimes allows ETF managers to adjust for market changes without directly selling portfolio securities (saving on capital gains taxes).

Asset Location, Location, Location!

Along with picking the most tax-efficient investments to lower your investment costs, you also want to choose the right types of accounts to hold your investments.

Asset location involves distributing specific assets between taxable, tax-deferred and tax-exempt accounts to minimize taxes and maximize your portfolio’s after-tax returns.

Learn more about asset location as an additional tool to reduce your overall investment costs.

Tax-Loss Harvesting

Tax-loss harvesting is a possible tax-minimization strategy also relating to investments within a taxable brokerage account.

It involves selling investments that have decreased in value or are underperforming, thereby realizing a capital loss, and replacing the investment with a highly correlated alternative. You would then use that loss to offset any realized capital gains from selling other investments, with the goal of reducing your overall tax liability.

If there are no realized capital gains to offset, up to $3,000 per year in investment losses can be used to offset your wages, taxable retirement income and other ordinary income (for married individuals filing separately, the deduction is $1,500).

With the NewRetirement Planner, you can review your potential tax burden in all future years and get ideas for minimizing this expense.

7. Looking for Professional Advice? You Have Low Cost Investing Options!

If you’re less of a DIY investor and prefer to get some professional guidance on your investment strategy, you can still manage to do so without paying high fees.

Assets Under Management Arrangement

Today, it’s still common for most financial advisors to be paid a fee based on a percentage of the assets they manage for you. This is referred to as an Assets Under Management (AUM) fee agreement.

This is likely one of the more expensive ways to work with a financial advisor. The typical AUM fee will average around 1% per year. So, if you have $500,000 invested with an advisor under an AUM arrangement, you are paying $5,000, and this fee could increase as your assets grow (although there can be tiered fees, depending on the advisor arrangement).

That’s a significant amount of money taken out of your investment returns each and every year, which can be avoided.

Flat Fee Arrangement

In order to avoid the high costs of receiving professional financial and investment advice under an AUM fee arrangement, you may want to consider a flat fee financial advisor.

By working with a flat fee financial planner, you will pay an agreed upon flat fee and be given an investment strategy that you can implement on your own. The advisor will typically help you with establishing an asset allocation based on your risk tolerance, even going as far as suggesting specific investments, but you would continue to have control over your investments and make the trades yourself.

In most cases, working with a flat fee financial advisor saves you a lot more money over the long-term vs. working with an AUM advisor.

Considering engaging a flat fee advisor? Partner with a CFP® professional from NewRetirement Advisors to define and reach your financial and investment goals. Book a FREE discovery session today.

Want to Save Costs Planning Your Financial Future? Start with NewRetirement Planner Today

Just as John Bogle championed low-cost investing, we at NewRetirement are dedicated to simplifying and making retirement planning more accessible and cost-effective for you.

Start or run a scenario in your NewRetirement Plan today.

Editor’s Note: Since he took over our Value Meter column in February, Director of Trading Anthony Summers has evaluated…

Copyright © 2024 Retiring & Happy. All rights reserved.